SIP vs. ULIP: Demystifying the Investment Landscape

Navigating the world of investments can feel like traversing a maze, especially with options like Systematic Investment Plans (SIPs) and Unit Linked Insurance Plans (ULIPs) vying for your attention. This article aims to provide a clear, neutral, and data-driven comparison to empower you to make informed decisions. For a deeper dive into SIPs, check out my book “Demystifying SIPs for Financial Freedom” available on Amazon and be sure to visit the Radha Consultancy YouTube channel for more insightful videos on various investment topics.

1. Core Purpose: Investing vs. Investing + Insurance

At their core, SIPs and ULIPs cater to distinct financial needs. A SIP is a disciplined approach to investing in mutual funds, designed purely for wealth accumulation. ULIPs, on the other hand, combine investment with life insurance. While this might seem convenient, it's crucial to understand the implications of this bundled approach. Often, the insurance coverage within a ULIP is inadequate, and a separate term insurance policy offers significantly better protection at a lower cost.

2. Cost Structure: The Impact on Your Returns

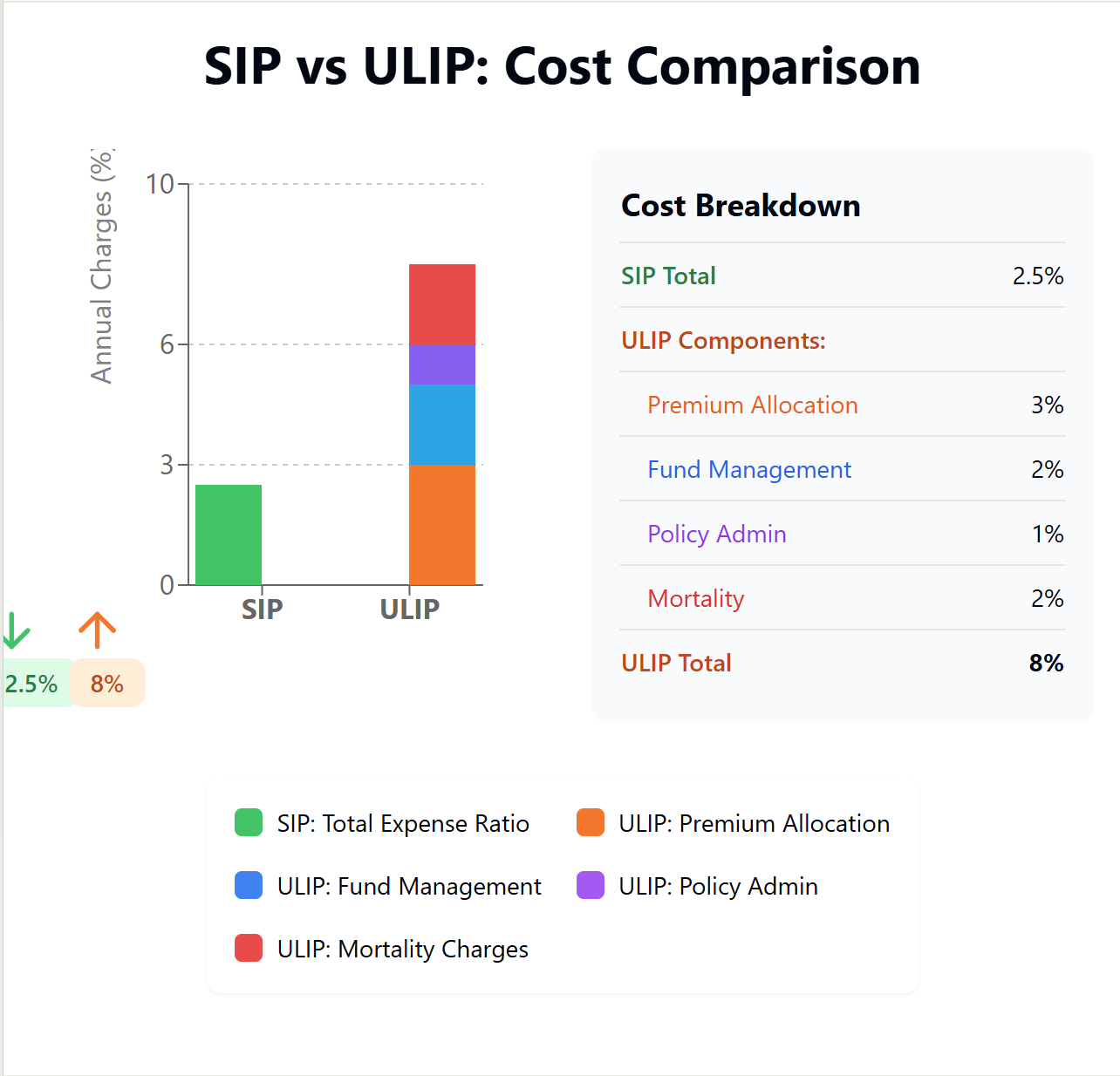

One of the most critical differences lies in their cost structures. SIPs have a transparent expense ratio, typically ranging from 0.5% to 2.5% annually, depending on the mutual fund. ULIPs, however, involve multiple charges: premium allocation charges (3-5% or more), policy administration charges (1-2% annually), mortality charges (which vary based on age and sum assured), and fund management charges (1.35-2.5%). These charges significantly impact your returns over the long term. For instance, over 15 years, a seemingly small difference of 2% in annual charges can lead to a substantially smaller final corpus. You can find illustrative calculations of the impact of charges in the following graphical representation. For more detailed examples, watch our latest video on the Radha Consultancy channel.

3. Flexibility & Control: Accessing Your Money

SIPs offer high liquidity and flexibility. You can withdraw your investments anytime (though some tax-saving ELSS funds have a 3-year lock-in). ULIPs, in contrast, usually have a 5-year lock-in period, and early withdrawals incur hefty surrender charges. Usually you will get back only 70% of the premium amount. SIPs also provide complete control over your fund choices and allow seamless switching between funds. ULIPs typically offer limited fund options and restricted switching. This flexibility is crucial for adapting to market changes and aligning your investments with your evolving financial goals.

Control & Transparency

SIP: Simplicity and Choice. ULIP: Complexity and Restrictions.

4. Returns: Market-Linked, but with a Catch

Both SIPs and ULIPs offer market-linked returns. However, due to the higher charges in ULIPs, their net returns are typically lower. For example, historical data suggests that SIPs in diversified equity funds have delivered average annual returns in the range of 12-15% over the long term, while ULIPs have averaged around 8-10%. (Remember, these are historical averages, and past performance is not indicative of future returns.) Want to see how these numbers play out in real-life scenarios? Head over to our YouTube channel, Radha Consultancy, for a deeper dive.

5. Tax Benefits: Understanding the Nuances

Both SIPs and ULIPs offer some tax benefits. Investments in ELSS mutual funds through SIPs qualify for deductions under Section 80C of the Income Tax Act, and long-term capital gains are also taxed favorably. ULIPs provide tax benefits under Section 80C for the premiums paid and Section 10(10D) for the maturity amount, subject to certain conditions. However, it's important to remember that tax benefits should not be the sole factor driving your investment decisions.

6. Other Features: Death Benefit, Surrender Value, and More

ULIPs provide a death benefit (sum assured) to your nominee, a feature not available with SIPs. However, it's often more cost-effective to opt for a separate term insurance plan for comprehensive life coverage. ULIPs also have a surrender value, but early withdrawals are penalized with surrender charges. Some ULIPs may offer loyalty additions as bonuses, but these rarely offset the impact of higher charges.

Conclusion:

Making the right investment choices is crucial for achieving your financial goals. While both SIPs and ULIPs have their place, SIPs, complemented by a term insurance plan, are generally a more efficient and cost-effective strategy for long-term wealth creation as given in the below table. For more personalized guidance, reach us for discussion. And don't forget to explore our other videos and resources on SIPs and other investment options on the Radha Consultancy YouTube channel!

Disclaimer: The information presented in this article is for educational purposes only and does not constitute financial advice. While data has been sourced using AI chatbots and publicly available information, ULIP and mutual fund scheme charges can vary significantly. The figures used are illustrative and intended to help explain the concepts involved. All market-linked investments are subject to market risk. Past performance is not indicative of future results.

Connect with Us

Kannan M

Consultant

"Unbiased Quality Advice"

Social Media

Subscribe to our Youtube channel

Blog - https://radhaconsultancy.blogspot.com/

LinkedIn : Connect with me on LinkedIn to learn more about my professional journey and insights.

FB Radha consultancy Page: Follow Radha Consultancy for updates on financial strategies and tips.

X Twitter : @KannanM1960 : Join the conversation on Twitter! Let's discuss finance, ebooks, and more.

Instagram : kannanm1994 : Get a glimpse into my world and the inspiration behind my writing.

#SIP #ULIP #Investment #MutualFunds #Insurance #PersonalFinance

No comments:

Post a Comment